How to Evaluate Income Riders on Annuities

Income riders have become one of the most discussed features in today’s annuity marketplace, especially for individuals focused on retirement planning and long‑term income guarantees. These riders—most commonly found on fixed indexed annuities—provide a way to create predictable, guaranteed lifetime income without giving up full control of the underlying contract’s value. But not all income riders work the same way, and understanding how to evaluate them is essential for making sound, informed financial decisions.

As part of my work at Financial Concepts in Celina, Ohio, I help clients navigate retirement planning, risk management, income planning, and wealth management decisions every day. This guide is designed to help you understand what income riders are, how they work, and what factors matter most when evaluating them.

Understanding What an Income Rider Is

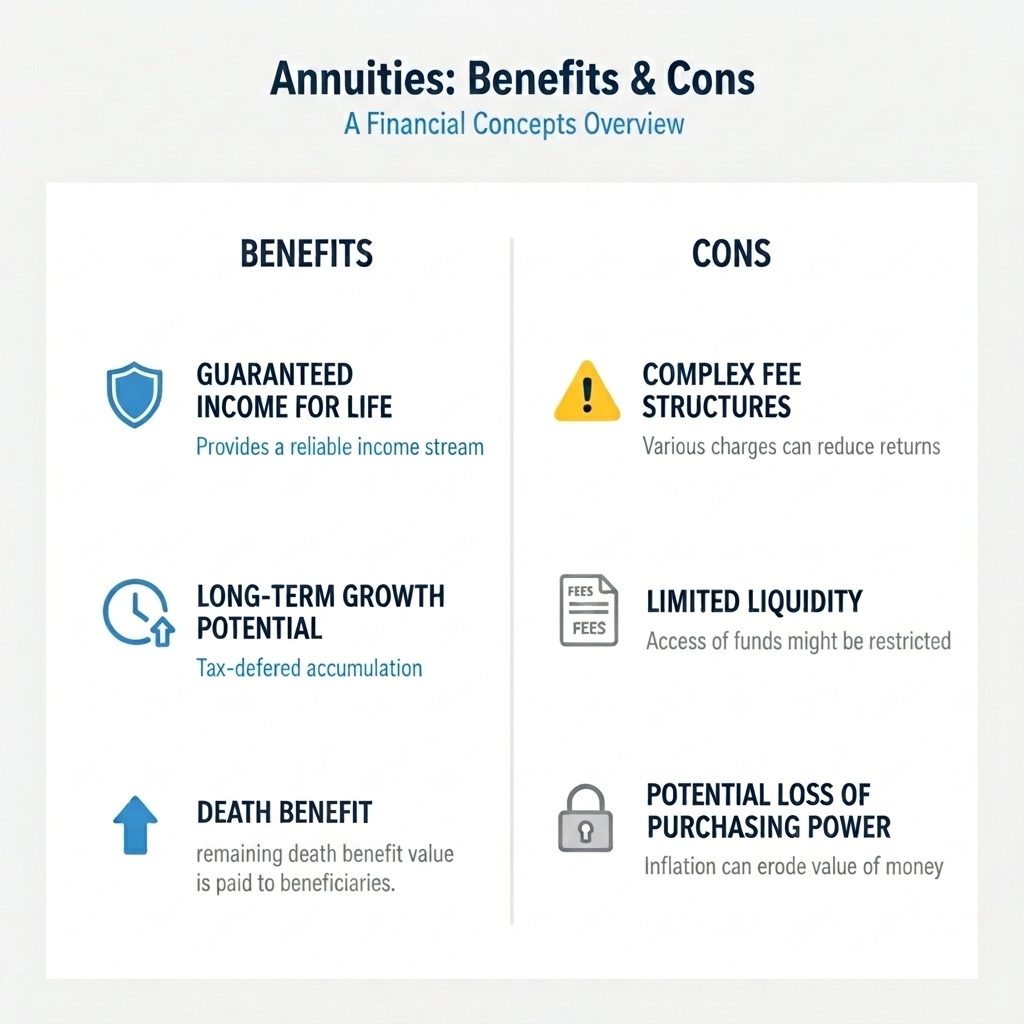

An income rider is an optional feature that can be added to certain annuities—typically fixed indexed annuities—to provide a guaranteed income stream in retirement. Unlike an immediate annuity that requires you to irrevocably hand over your principal in exchange for income, an income rider allows the annuity to continue growing while you maintain access to the contract’s value.

The rider usually comes with an annual cost, but in exchange, it offers:

- Guaranteed lifetime income

- A predictable growth rate used for income calculations

- A source of income unaffected by market volatility

- The ability to defer income until the time is right

Income riders can be highly effective for clients seeking a source of stability in their retirement income planning—especially those who want the benefits of guaranteed income without fully annuitizing their funds.

The Two “Values” Inside an Income Rider

A key area of confusion with income riders is the existence of two different values within the contract:

1. The Account Value: This is the actual value of your annuity—the amount you could walk away with if you surrendered the contract or used the funds for another purpose. The account value is tied to interest credits and can fluctuate based on the annuity’s features.

2. The Income Benefit Base: This is a virtual value used only to calculate your lifetime income. It is not a cash value and cannot be withdrawn. The income base often grows at a guaranteed rate—commonly described as a “roll‑up rate”—until you start taking income.

Understanding the difference between these two values is essential because many riders advertise attractive growth rates that apply only to the income base, not the actual account value.

Key Factors to Evaluate in an Income Rider

Income riders vary widely, so evaluating them properly requires looking at the contract’s guarantees, costs, and suitability within your broader retirement planning goals. Here are the most important factors:

1. The Cost of the Rider

Income riders usually charge an annual fee in the form of a deduction of the annuity's account value. The fee often ranges from 0.75% to 1.50% of the account value. While this cost provides lifetime income guarantees, it must be weighed against your broader financial planning strategy, including income needs, tax planning, and long‑term goals.

Be sure to evaluate:

- The annual rider cost

- Whether the cost is fixed or variable

- How the fee impacts the contract’s account value over time

2. The Guaranteed Roll‑Up Rate

The roll‑up rate determines how quickly the income benefit base grows before income begins. Some riders offer a guaranteed rate for a certain number of years; others allow the income base to grow based on market index performance.

Important questions to ask include:

- Is the roll‑up rate guaranteed?

- For how many years does it apply?

- Does it continue after income begins, or does it stop?

3. Payout Percentages

Your lifetime income is determined by multiplying the income benefit base by a payout percentage, which is typically based on your age when income begins. These percentages often increase over time, rewarding those who wait longer before starting income.

When evaluating payout percentages, consider:

- Your planned retirement age

- How payout bands change with age

- Whether the payout is single life or joint life

4. Flexibility of Income

Not all riders offer the same flexibility. Some allow you to pause or reduce income; others lock in the payout once it starts. Flexibility can be important if your income needs vary from year to year.

5. Inflation Adjustments

Some income riders allow income to increase over time if the underlying index performs well, while others offer level income. For many retirees, inflation adjustments, whether built‑in or market‑linked, can be a significant factor when planning decades of retirement. Keep in mind that some inflation adjustment features aren't automatically included in an income rider. They may be offered as a separate rider with it's own fee. Be sure to thoroughly review the terms and costs associated with inflation adjustment features before purchase.

6. Spousal Options

If you are married, consider how the rider treats joint income. Many riders offer joint options, allowing income to continue for the surviving spouse. Costs and payout percentages can differ for joint life riders, so it is important to understand those distinctions.

7. Financial Strength of the Carrier

Because annuity guarantees rely on the claims-paying ability of the issuing insurance company, evaluating the insurer’s financial strength is a critical part of assessing any income rider. Independent ratings—such as AM Best or Standard & Poor’s—can provide insight into an insurer’s ability to meet long‑term obligations.

Evaluating Whether an Income Rider Fits Your Financial Plan

An income rider is most effective when it aligns with a broader retirement income strategy rather than being used in isolation. At Financial Concepts, I work with clients to determine whether an income rider fits into their overall income planning, risk management, and retirement planning goals.

An income rider may be a fit if you:

- Want predictable, guaranteed lifetime income

- Prefer to defer income for several years to increase benefits

- Need a source of income that you won't outlive

- Want income without losing access to the underlying account value

It may be less suitable if you expect to rely more heavily on portfolio withdrawals, have a short time horizon, or do not need guaranteed income.

FAQ

Do income riders guarantee income for life?

Most income riders provide guaranteed lifetime income once activated. This protection can be valuable for retirees concerned about outliving their assets. Be sure to review the terms of an income rider to confirm that the income is guaranteed for life and not only for a specified period of time.

Can I withdraw the income benefit base?

No. The income benefit base is not a cash value; it is only a calculation value used to determine lifetime income.

Do income riders increase the value of my annuity?

Not directly. The rider’s roll‑up rate applies to the income benefit base, not the actual account value. Income riders are designed for income guarantees, not enhanced cash value.

Can I cancel an income rider?

Some riders allow cancellation, while others remain in place for the life of the contract. It depends on the annuity’s terms.

Are income riders worth the cost?

They can be—especially for clients who want guaranteed income and plan to use the rider. The value depends on your income needs, time horizon, and overall financial plan.

Can a withdraw from the annuity's account value affect an income rider?

Possibly, it depends on the terms of the annuity contract and rider. Taking a withdraw from the annuity's account value could reduce the amount of guaranteed income the rider provides. Be sure to thoroughly review an annuity and an income rider's terms and conditions before purchasing an annuity contract and rider, and prior to taking any withdraws to determine how the withdraw can affect the rider, the account value, your tax situation, and if any surrender charges could be triggered as a result of the withdraw.

Equity-indexed annuities may not be suitable for all investors. You should consult a licensed insurance agent regarding your financial objectives and unique situation to help determine if an equity-indexed annuity is right for you. Please make sure you review all marketing materials, specimen contracts, buyer’s guides, and forms related to the annuity to ensure that it is appropriate based on your short-term and long-term financial situation and liquidity needs. Withdrawals may be subject to income tax, and a 10% federal income tax penalty may apply to withdrawals before age 59½. Additionally, certain charges (referred to as “surrender charges”) may apply if you withdraw more than the penalty-free amount in a given year. Under current law, tax deferral is a basic feature of tax-qualified plans. Placing qualified funds into an annuity does not provide any additional tax benefit. Unlike CDs, equity-indexed annuities are not insured by the FDIC. Investors can lose principal if an equity-indexed annuity is terminated prior to the end of the surrender period. Some equity-indexed annuities guarantee a minimum interest rate of 0%. Features such as participation rates, rate caps, and spread/asset/margin fees may change over time and adversely affect your return if an insurance company subsequently lowers the participation rate or cap or increases the spread/asset/margin fees. The principal guarantee and income for life guarantee features of equity-indexed annuities are subject to the claims-paying ability of the issuing insurance company. If you take an early distribution from an annuity you may be subject to a surrender charge which could result in a loss of principal. You may also be subject to a tax penalty if you make a withdrawal before age 59½.